Why Your Best Employees May Be Burning Out Mid-Year

Burnout isn’t always obvious. Learn why your highest-performing employees are often the most at risk, the warning signs managers miss, and how better workload design can help prevent burnout before it impacts retention and performance.

Should You Change Jobs or Stay Put? Understanding Job Hopping vs Job Hugging

Should you stay with your current employer or look for a new opportunity? This guide explores the differences between job hopping and job hugging, helping professionals make informed career decisions while giving employers valuable insights into employee retention.

Are Your Labour Costs Driving Profit or Inefficiency This EOFY?

Most EOFY conversations focus on tax deductions and refunds. But what if the bigger profitability issue is hiding in your labour costs? Learn how rising employment expenses, administrative bottlenecks, and inefficient team structures may be costing your business more than you realise.

How to Build Team Culture With Offshore and Remote Teams

Building a strong culture with offshore and remote teams takes more than workflows and productivity metrics. From team outings and company events to recognition and connection, discover how businesses can improve engagement, retention, and performance by creating a workplace people genuinely want to be part of.

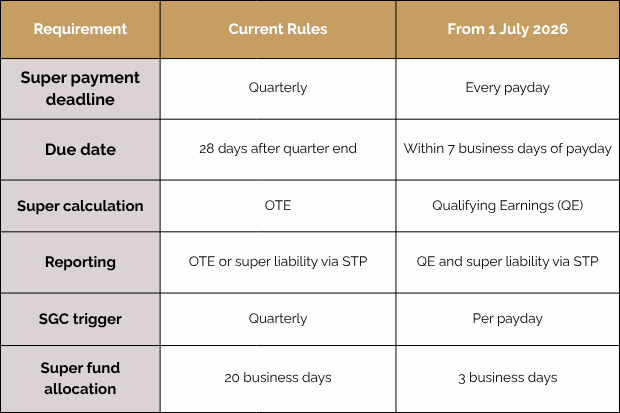

What Payday Super Means for Financial Advisers and Business Owners

The new Payday Super rules will require employers to pay super alongside wages from July 2026. Discover what the changes mean for compliance, cash flow, payroll processes, and business operations.

Will AI Take Our Jobs? What Workers Should Actually Be Worried About

AI is rapidly changing how businesses operate, but will it actually replace workers? Explore which jobs are most vulnerable, how AI is reshaping industries, and the skills professionals need to stay valuable.

One Response